Ask ten people what wealth management means, and nine will likely describe a financial advisor overseeing investments for a wealthy individual. The tenth person is usually someone who has worked within a family office or multi-generational wealth structure. They will tell you that wealth management is far broader.

Wealth management for affluent families is the coordinated stewardship of significant assets. It covers investments, taxation, legal structuring, estate planning, insurance, philanthropy, and governance. It comes into play when the complexity of substantial wealth extends beyond what any single product, advisor, or strategy can effectively manage on its own. This distinction is critical. Families who view wealth management as nothing more than advanced investing often make a fundamental error in judgment, with consequences that tend to emerge at the most critical moments — such as death, divorce, liquidity events, or the transfer of inheritance.

The foundation: Clarity before strategy

For an affluent family, this baseline exercise often reveals surprises: assets more concentrated than assumed, insurance coverage insufficient relative to current net worth, or estate documents reflecting a family situation that no longer exists. The family that completed its estate planning in 2005 and has never revisited it is, in financial terms, navigating with an outdated map.

The first act of wealth management is clarity. And clarity is rarer than wealth.

Investment strategy: Beyond the portfolio

Investment management at the wealth level is fundamentally different from retail investing, not in principle, but in scope, access, and consequence. The objective shifts from maximizing returns to achieving specific, defined outcomes: funding a lifestyle, endowing a foundation, capitalizing a next-generation entrepreneur, or preserving purchasing power across thirty years of inflation.

At the affluent level, the investment universe expands significantly. Public equities and fixed income represent only a portion of what a properly structured wealth portfolio contains. Private equity, direct real estate, venture capital, private credit, hedge strategies, commodities, and infrastructure become material allocations.

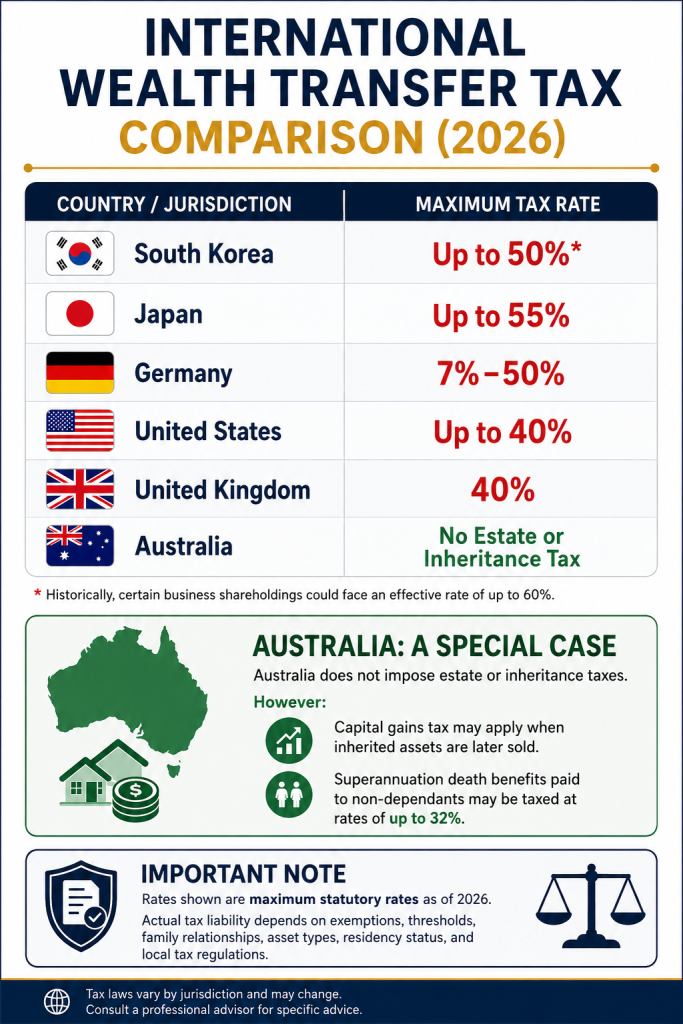

Tax optimization: The invisible return

At significant wealth levels, tax planning is not a compliance function, it is one of the highest-return activities available to a family. The difference between a tax-efficient and tax-inefficient structure on a $20 million estate can be measured in millions of dollars over a generation, without any difference in investment performance whatsoever.

The instruments of tax optimization go far beyond annual returns.

These include:

- Entity structuring — holding companies, partnerships, and trusts that change the legal character of income and gains.

- Cross-border planning for families with assets or members in multiple countries.

- Charitable structures that convert tax liability into philanthropic impact. And they include long-range planning for the ultimate tax event: the transfer of wealth at death.

Estate and succession planning: The real test

If investment management is the engine of wealth, estate planning is the transmission. The structure that determines whether what has been built is successfully and fully passed on to the next generation.

Research frequently cited in wealth-management circles suggests that approximately 70% of wealthy families fail to preserve their wealth into the second generation, with nearly 90% seeing significant erosion by the third. While these figures are debated and vary by definition, advisers consistently note that wealth loss is often driven less by investment performance alone and more by inadequate succession planning, family conflict, weak governance, and insufficient preparation of heirs.

The core estate planning instruments

Wills and testamentary documents The baseline legal statement of distribution intent. Necessary but insufficient at significant wealth levels — subject to probate, public disclosure, and contestation without additional structuring.

Revocable and irrevocable trusts Legal structures that hold assets outside the taxable estate, control distribution timing and conditions, protect assets from creditors and divorce proceedings, and bypass probate entirely. The irrevocable trust, once established, removes assets from the grantor’s estate permanently — a powerful but irreversible tool.

Family limited partnerships and holding companies Corporate structures that consolidate family assets under unified ownership, facilitate valuation discounts for gifting purposes, and provide legal separation between personal and business assets — critical for families with operating businesses.

Life insurance as a wealth transfer tool At the affluent level, life insurance is frequently not about income replacement — it is about estate liquidity. An irrevocable life insurance trust can provide heirs with the tax-free capital needed to pay an estate tax bill without forcing the sale of illiquid assets like real estate, business interests, or art.

Succession planning for family businesses When a family’s wealth is concentrated in an operating business, the succession question — who leads it, who owns it, how it is valued for transfer purposes — is often the single most consequential financial decision of a generation.

Family governance: The dimension no one talks about

Of all the disciplines within wealth management, governance is the least understood and the most consequential. Family governance is the set of structures, agreements, and processes by which a family makes decisions about shared wealth — who has authority, on what terms, through what process, and according to what values.

“The families that lose their wealth in the second generation almost never lose it to a market crash. They lose it to a disagreement that no one had the structure to resolve.”

The formal instruments of family governance include:

- The family constitution — a document that articulates the family’s values, investment philosophy, and decision-making rules

- The family council — a regular, structured meeting to discuss shared financial matters

- Financial education programs — preparing younger generations for the responsibilities they will one day assume

- Conflict resolution mechanisms — determining what happens when family members disagree about material financial decisions

Families that invest in governance consistently preserve more wealth than those who invest only in investment management.

The only question that matters

Wealth management, at its deepest level, is the answer to a single question that every affluent family must eventually confront: what is this wealth for?

Families that articulate a clear purpose, philosophy, and set of values to guide the use and transfer of wealth consistently preserve more across generations than those who view wealth solely through a financial lens.

Because at the highest level of complexity, wealth management is not fundamentally a financial discipline — it is a human one.

The instruments may be sophisticated. The strategies may be complex. The advisers may be highly specialized. Yet the foundation of every successful multi-generational wealth structure remains remarkably consistent: a family that understands what it stands for and has built the legal, financial, and governance framework to protect that legacy across time.

👉 Book a consultation with one of our Cross-Border Financial Advisors today.

MEET THE ASTRA WORLDWIDE ADVISORS

Email: inquiry@astraworldwide.com

www.astraworldwide.com

Securing your future together!

______________________________________________________________________________________________

Follow us on

LinkedIn | Facebook | YouTube | Instagram

______________________________________________________________________________________________

Related Insights: